Why Most 401(k) Millionaires Still Lose the Retirement Game (And How the Roth Conversion Excelerator Can Secure What Wall Street Can’t)

Discover how the Roth Conversion Excelerator strategy turns your 401(k) or IRA into tax-free retirement income with 0% market risk and a $1M+ legacy for heirs..

Rakesh Shah

6/13/20253 min read

You’ve worked hard, saved aggressively, and now you’ve got $400,000… $800,000… maybe even $1 million+ sitting in your 401(k), IRA, or other retirement account. So why are financial professionals warning that you still may lose the retirement game?

Let’s break it down.

📉 The Hidden Risks in “Traditional” Retirement Accounts

Most people assume that if their 401(k) or IRA grows at 8–10% annually, they’re golden.

But here’s what rarely gets discussed:

✅ Every dollar is fully taxable when you take it out

✅ Required Minimum Distributions (RMDs) force withdrawals at 73+ — whether you need the money or not

✅ Higher income in retirement can trigger IRMAA penalties, raising your Medicare premiums

✅ If you pass away, your kids must drain the account within 10 years — and often lose 30%–40% of the value to taxes

Even if you manage to grow your portfolio well, the IRS is quietly partnered with you — and they're set to collect.

💼 But I Can Outperform the Market, Right?

Some investors feel confident they’ll earn 15–20% per year. That’s impressive — but it’s also worth a reality check.

The S&P 500 has averaged ~10% annually since the 1980s

The average investor earns ~6–7%, due to emotional investing and market timing (DALBAR study)

Even top hedge funds and RIAs aim for 8–12%, net of fees

And 401(k) plans often have limited fund options and fees that reduce performance

So unless you're beating Warren Buffett and running your own trading desk, odds are… you won’t hit 15% every year for 20+ years — and you still face taxes on the backend.

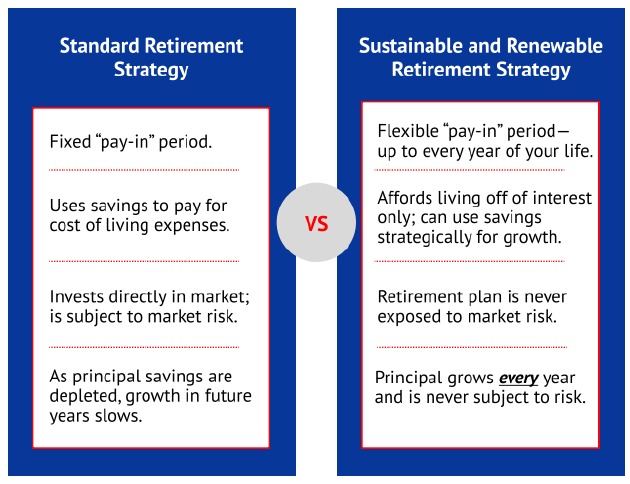

🔐 The Roth Conversion Excelerator Strategy: Tax-Free. Risk-Free. Legacy-Protected.

Here’s what a coordinated team of CPAs, Investment Advisor Representatives (IARs), fiduciaries, and major insurance institutions are quietly helping their high-net-worth clients implement:

The Roth Conversion Excelerator is a fully structured, tax-advantaged retirement strategy designed to reposition a portion of your qualified or non-qualified assets into:

✅ Tax-free retirement income with built-in income guarantees

✅ 0% market risk and full principal protection, backed by top-rated financial institutions

✅ Lifetime income structured under regulatory-backed, contractual guarantees

✅ Income you can never outlive

✅ A $1M+ tax-free legacy passed to your heirs

✅ Freedom from RMDs, IRMAA penalties, and rising tax bracket exposure

This isn’t a product — it’s a strategic shift: converting taxable, uncertain assets into tax-free, reliable income and preserved generational wealth.

💰 Real Example (Based on Actual Client Scenario)

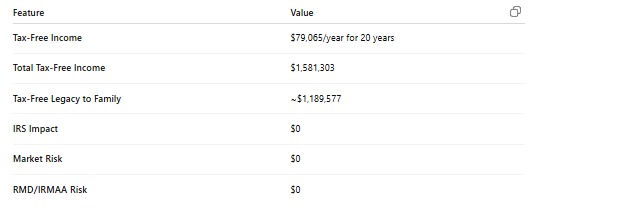

Let’s say you're 50 years old (income begins at age 65) and reposition $500,000 from your IRA or 401(k) into the Roth Excelerator strategy.

👉 These are intentionally conservative projections based on a 7% indexed return model. Your actual outcome may vary based on your specific situation — and in many cases, results can be even stronger depending on timing, age, and structure.

If you wait until age 70 to begin taking income, the projected payout could grow to $127,243/year for 20 years or more — still tax-free.

Now ask yourself: What would you need to consistently earn in a taxable investment to match that same $79,000/year after taxes?

Answer: Over $123,000/year in taxable income — consistently — just to keep pace.

🧠 Why This Works (And Why It’s Gaining Attention)

It uses structured tax code strategies, indexed growth, and insurance-based vehicles that are legally designed to grow and distribute money tax-free

It’s actively managed by fiduciary IARs, tax advisory teams, and vetted insurance carriers

It avoids the landmines of RMDs, tax hikes, and sequence of return risk

And it’s backed by some of the strongest financial institutions in the country

🧭 Not a Replacement. A Smart Parallel Strategy.

This isn’t about replacing your 401(k) or firing your financial advisor.

It’s about creating a parallel track:

One that’s tax-free, stress-free, and guaranteed — no matter what happens with markets, taxes, or policy.

🚀 Who Is This For?

This may be a fit for you if:

You have $600,000+ in a qualified account (401k, IRA, SEP, etc.)

OR $100,000+ in a non-qualified brokerage account or bank savings

You’re age 35–70, and want more control, tax savings, and legacy value

You want to protect your retirement income from taxes, inflation, and market downturns

📩 Ready to See What This Could Look Like for You?

No pressure. No cost. Just numbers.

Or request your personalized Roth Conversion Excelerator Summary — and see the tax-free income and legacy value that’s possible for your family.